In my last two posts (Part 1 and Part 2), I explored time series forecasting with the timekit package.

In this post, I want to compare how Facebook’s prophet performs on the same dataset.

Predicting future events/sales/etc. isn’t trivial for a number of reasons and different algorithms use different approaches to handle these problems. Time series data does not behave like a regular numeric vector, because months don’t have the same number of days, weekends and holidays differ between years, etc. Because of this, we often have to deal with multiple layers of seasonality (i.e. weekly, monthly, yearly, irregular holidays, etc.). Regularly missing days, like weekends, are easier to incorporate into time series models than irregularly missing days.

Timekit uses a time series signature for modeling, which we used as features to build our model of choice (e.g. a linear model). This model was then used for predicting future dates.

Prophet is Facebook’s time series forecasting algorithm that was just recently released as open source software with an implementation in R.

“Prophet is a procedure for forecasting time series data. It is based on an additive model where non-linear trends are fit with yearly and weekly seasonality, plus holidays. It works best with daily periodicity data with at least one year of historical data. Prophet is robust to missing data, shifts in the trend, and large outliers.”

(I am not going to discuss forecast and ARIMA or other models because they are quite well established with lots and lots of excellent tutorials out there.)

Training and Test data

I am using the same training and test intervals as in my last post using timekit.

Just as with timekit, prophet starts with a data frame that consists of a date column and the respective response variable for each date.

library(prophet)

library(tidyverse)

library(tidyquant)

retail_p_day <- retail_p_day %>%

mutate(model = ifelse(day <= "2011-11-01", "train", "test"))

train <- filter(retail_p_day, model == "train") %>%

select(day, sum_income) %>%

rename(ds = day,

y = sum_income)

test <- filter(retail_p_day, model == "test") %>%

select(day, sum_income) %>%

rename(ds = day)

Model building

In contrast to timekit, we do not “manually” augment the time series signature in prophet, we can directly feed our input data to the prophet() function (check the function help for details on optional parameters).

To make it comparable, I am feeding the same list of irregularly missing days to the prophet() function. As discussed in the last post, I chose not to use a list of holidays because the holidays in the observation period poorly matched the days that were actually missing.

off_days <- data.frame(ds = as.Date(c("2010-12-24", "2010-12-25", "2010-12-26", "2010-12-27", "2010-12-28",

"2010-12-29", "2010-12-30", "2010-01-01", "2010-01-02", "2010-01-03",

"2011-04-22", "2011-04-23", "2011-04-24", "2011-04-25", "2011-05-02",

"2011-05-30", "2011-08-29", "2011-04-29", "2011-04-30"))) %>%

mutate(holiday = paste0("off_day_", seq_along(1:length(ds))))

prophet_model_test <- prophet(train,

growth = "linear", # growth curve trend

n.changepoints = 100, # Prophet automatically detects changes in trends by selecting changepoints from the data

yearly.seasonality = FALSE, # yearly seasonal component using Fourier series

weekly.seasonality = TRUE, # weekly seasonal component using dummy variables

holidays = off_days)

## Initial log joint probability = -8.3297

## Optimization terminated normally:

## Convergence detected: relative gradient magnitude is below tolerance

Predicting test data

With our model, we can now predict on the test data and compare the predictions with the actual values.

forecast_test <- predict(prophet_model_test, test)

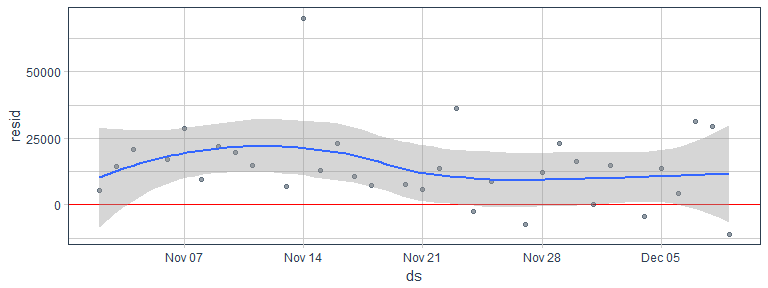

Just as with timekit, I want to have a look at the residuals. Compared to timekit, the residuals actually look almost identical…

forecast_test %>%

mutate(resid = sum_income - yhat) %>%

ggplot(aes(x = ds, y = resid)) +

geom_hline(yintercept = 0, color = "red") +

geom_point(alpha = 0.5, color = palette_light()[[1]]) +

geom_smooth() +

theme_tq()

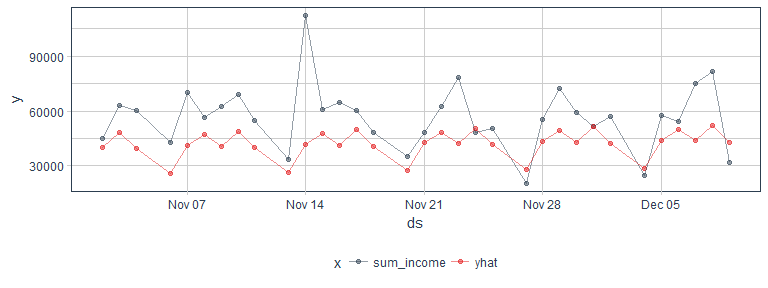

… As does the comparison plot. So, here it seems that prophet built a model that is basically identical to the linear model I used with timekit.

forecast_test %>%

gather(x, y, sum_income, yhat) %>%

ggplot(aes(x = ds, y = y, color = x)) +

geom_point(alpha = 0.5) +

geom_line(alpha = 0.5) +

scale_color_manual(values = palette_light()) +

theme_tq()

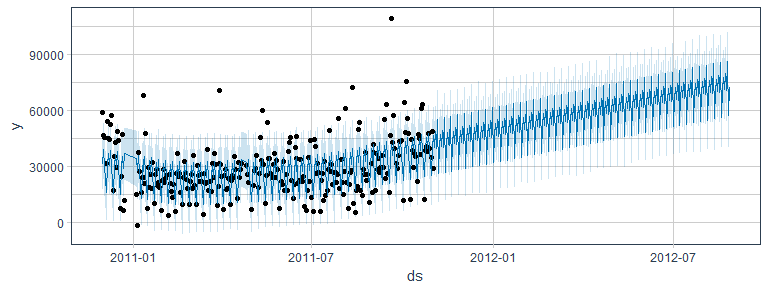

Predicting future sales

Now, let’s see whether the future predictions will be identical as well.

Just like with timekit, I am using a future time series of 300 days. Here, we see a slight difference in how we generate the future time series: with timekit I could use the entire index of observed dates, together with the list of missing days, while prophet uses the forecasting model that was generated for comparing the test data, i.e. it only considers the dates from the training set. We could built a new model with the entire dataset but this would then be different to how I approached the modeling with timekit.

future <- make_future_dataframe(prophet_model_test, periods = 300)

forecast <- predict(prophet_model_test, future)

plot(prophet_model_test, forecast) +

theme_tq()

Interestingly, prophet’s forecast is distinctly different from timekit’s, despite identical performance on test samples! While timekit predicted a drop at the beginning of the year (similar to the training period), prophet predicts a steady increase in the future. It looks like timekit put more weight on the overall pattern during the training period, while prophet seems to put more weight on the last months, which showed a rise in net income.

sessionInfo()

## R version 3.4.0 (2017-04-21)

## Platform: x86_64-w64-mingw32/x64 (64-bit)

## Running under: Windows 7 x64 (build 7601) Service Pack 1

##

## Matrix products: default

##

## locale:

## [1] LC_COLLATE=English_United States.1252

## [2] LC_CTYPE=English_United States.1252

## [3] LC_MONETARY=English_United States.1252

## [4] LC_NUMERIC=C

## [5] LC_TIME=English_United States.1252

##

## attached base packages:

## [1] stats graphics grDevices utils datasets methods base

##

## other attached packages:

## [1] tidyquant_0.5.1 quantmod_0.4-8

## [3] TTR_0.23-1 PerformanceAnalytics_1.4.3541

## [5] xts_0.9-7 zoo_1.8-0

## [7] lubridate_1.6.0 dplyr_0.5.0

## [9] purrr_0.2.2.2 readr_1.1.1

## [11] tidyr_0.6.3 tibble_1.3.1

## [13] ggplot2_2.2.1 tidyverse_1.1.1

## [15] prophet_0.1.1 Rcpp_0.12.11

##

## loaded via a namespace (and not attached):

## [1] rstan_2.15.1 reshape2_1.4.2 haven_1.0.0

## [4] lattice_0.20-35 colorspace_1.3-2 htmltools_0.3.6

## [7] stats4_3.4.0 yaml_2.1.14 rlang_0.1.1

## [10] foreign_0.8-68 DBI_0.6-1 modelr_0.1.0

## [13] readxl_1.0.0 plyr_1.8.4 stringr_1.2.0

## [16] Quandl_2.8.0 munsell_0.4.3 gtable_0.2.0

## [19] cellranger_1.1.0 rvest_0.3.2 codetools_0.2-15

## [22] psych_1.7.5 evaluate_0.10 labeling_0.3

## [25] inline_0.3.14 knitr_1.16 forcats_0.2.0

## [28] parallel_3.4.0 broom_0.4.2 scales_0.4.1

## [31] backports_1.0.5 StanHeaders_2.15.0-1 jsonlite_1.5

## [34] gridExtra_2.2.1 mnormt_1.5-5 hms_0.3

## [37] digest_0.6.12 stringi_1.1.5 grid_3.4.0

## [40] rprojroot_1.2 tools_3.4.0 magrittr_1.5

## [43] lazyeval_0.2.0 xml2_1.1.1 extraDistr_1.8.5

## [46] assertthat_0.2.0 rmarkdown_1.5 httr_1.2.1

## [49] R6_2.2.1 nlme_3.1-131 compiler_3.4.0